Rounded Citizen Lending Academy

The Complete Guide to Understanding Mortgages

Mortgages are a complicated product with many moving parts. Even those who have gone through the process of buying a home many times still find the mortgage part confusing and challenging. Our comprehensive guide will address all of your questions and will empower you to make smarter decisions.

Jump Forward To:

Home » The Complete Guide to Understanding Mortgages

Advertiser Disclosure

Tooltip contentBasics of Mortgages

In this section, we explain what a mortgage is, go over all you need to know regarding the mortgage interview and documents and list out general requirements associated with qualifying for a mortgage.

What is a Mortgage?

A mortgage is a type of loan that is secured by real estate. To put it even simpler, a mortgage is a loan you use to buy a home. You promise to pay the lender back in exchange for funds to purchase a home.

If you fail to keep your promise to pay the lender back, you’ll default on your loan and the lender will be forced to “foreclose” on your home (more on this later).

Undoubtedly, purchasing a home will be one of the most important purchases (if not the most important) that you will make during the course of your life. The decision to stop renting and buy can lead to greater financial responsibility and control. There is just something about owning rather than renting that makes people more responsible. But, becoming a homeowner is a BIG step and you should approach it very carefully.

You probably have a lot of questions or have heard confusing terms like escrow, pre-approval, points, and much more. Don’t worry, we have your back. We promise to answer all of your questions and address any concerns that you might have.

Interview & Documents

The first thing you need to do is get in touch with a mortgage lender. This can be the financial institution where you do your regular banking, another local bank, an online mortgage lender, or credit union.

Do not stress the initial meeting with your lender, it’s simply a get-to-know-you. Remember, the lender needs your business. Never feel like you can’t ask a question. The lender is there to get to know you and your financial standing and you’re there to find out as much as possible!

Rounded Citizen Pro Tip

Credit Unions are known for having low rates and a very hands-on approach! We recommend you find a local credit union and work with them.

Remember, unlike an auto loan, mortgages require A LOT of paperwork. It is a good practice to have the following documents ready whenever the lender requests it:

- Income Documents

- Tax Returns

- Asset Statements

- Sales Agreement

- W-2 Employed – Bring TWO most recent paystubs

- Social Security Income – Current year Social Security statement (If it applies to you)

- Retirement Income – Pension statement (If it applies to you)

- Self-Employed – Business Returns (including all schedules)

- Just to be safe, bring copies of the last TWO years (including all schedules)

- W-2’s & 1099’s

- Personal bank statements

- 401(k) statements

- Other investment account statements

- This is the document that outlines the terms of the real estate purchase transaction between you and the seller.

Don’t worry if you don’t have everything that is listed above. By the end of the initial interview, a good lender will go over in great detail what documents you need for your particular mortgage loan. Besides, the lender is NOT allowed to request any documents from you until the “Intent to Proceed” document is signed. Signing the Intent to Proceed document means that after shopping a few lenders, you have finally decided to proceed with one.

Another thing to keep in mind is that if any lender is giving you a hard time, you can always go to another lender. There are hundreds of great lenders out there! Never proceed with a lender if you don’t understand something!

Affordability

How much can I afford? That’s the golden question that every prospective home buyer asks themselves. Use this intuitive calculator to figure out exactly how much home you qualify for!

-

Your Income & Monthly Debts

This one is obvious, the home you can afford largely depends on your monthly income & liabilities. At Rounded Citizen, we recommend keeping your monthly housing payment to 20 - 25% of your monthly gross income. For example, if you earn $6,000 a month, your monthly mortgage payment should be no more than $1,500. Try not to go higher. The higher you go, the more your home turns into a liability rather than an asset! When lenders review a loan, they strictly look at something called Debt-To-Income or DTI for short. For example, if your monthly liability (credit cards, auto loans, student loans, and housing payment) is $2,100 and your monthly gross income is $6,000, your DTI ratio is 35%. For most lenders in the USA, the maximum DTI is 43%.

-

Down Payment

A home down payment is simply the part of the home purchase price that you pay upfront. This is the part that the lender does not finance via mortgage. We recommend at the very least of making a down payment of 5%. But remember, putting down less than 20% will result in you having to pay PMI (more on PMI below). Deciding the amount to use as a downpayment varies from situation to situation. Be careful when taking advice from someone that is not a licensed professional in the field. Always assess your individual financial standing and consult with your mortgage lender.

-

Closing Costs

Closing costs are fees that you pay in order to obtain your loan. Closing costs can include lender fees, title company fees, tax/government fees, escrow payments, and other miscellaneous fees. The total cost to close on a loan varies, but usually, it's 2 - 5% of the loan amount. Often, when individuals save to purchase a home, they forget about the hefty fees that come with closing on a mortgage. When negotiating with the seller on the purchase price of a home, ask your realtor to negotiate in "seller assist". Seller assist will help cover a portion or all of your closing costs.

-

Property Taxes

Property tax is exactly what it sounds like. It's a tax that is assessed on real estate. Property taxes are paid on a yearly, semi-annually, or quarterly basis. Property taxes allow your local government to pay for schools, police, fire departments, roadwork, and other local services. Depending on the size of your downpayment, your lender will either require (downpayment <20%) or allow you to open up an escrow account to cover your property tax payments. To put it simply, instead of you having to make a large property tax payment yourself, your lender will collect a smaller portion from you monthly and will make the property tax payment(s) on your behalf.

-

Homeowners & Flood Insurance

Homeowners insurance is a type of insurance that covers your primary residence. Flood insurance is a specific kind of coverage against loss due to flooding. Depending on the size of your downpayment, your lender will either require (downpayment <20%) or allow you to open up an escrow account to cover your insurance premium(s). To put it simply, instead of you having to make a large insurance payment yourself, your lender will collect a smaller portion from you monthly and will make the payment(s) on your behalf.

-

PMI

Private Mortgage Insurance or PMI is an insurance policy that protects the lender in the event that you default on your loan. Remember, PMI does not protect you, only the lender. Usually, the PMI payment is added onto your monthly mortgage payment and it ranges anywhere from $30 - $500 a month. There are two ways to cancel a PMI premium. You can pay down your mortgage to below 80% of the original loan amount, which will result in the lender automatically cancelling the PMI premium. Or, by contacting the lender and asking them to order an appraisal on your behalf. If the value of your home is high enough, the lender will cancel the PMI premium. We suggest getting in touch with your lender and asking about their specific procedures on handling PMI premiums.

-

HOA

A homeowner's association or HOA is an administration in a subdivision, planned development, or condominium building. The HOA is responsible for enforcing rules, keeping all common areas clean, and often covers trash removal and water fees. An HOA can be a blessing or a curse. It varies from place to place. The most important factor to remember is that HOA's always come with a fee attached. The fee can range anywhere from $30, all the way up to $1,000.

Required Credit Score for Mortgages

What is my credit score? How does my credit score affect the rate I will receive? These are all important questions that you might be asking yourself.

Lenders consider your credit score to be one of the most important factors when trying to obtain a mortgage. Your credit score can affect the following:

- Annual Percentage Rate (APR)

- Required Downpayment

- Loan Program

- Loan Amount

Before applying for a mortgage, it’s good practice to check your credit score. In today’s market, there is a myriad of free credit score providers! Some of our favorites are credit karma, annual credit report, and Experian. Using one of these free credit score providers or even a combination of all three will help with discovering and resolving any potential credit issues that you might have.

Credit Score, APR, and Payment Breakdown (Example)

We utilized myFICO.com to showcase how much a borrower can save on their mortgage payment just by having a higher credit score. The below example shows that borrowers with an above 760 credit score save as much as $219 per month on a 30-year fixed, $250,000 mortgage compared with borrowers that carry a score ranging from 620-639. To put that in a perspective, if you make regular monthly payments over a 30-year period, borrowers with a score ranging from 620-639 can expect to pay $78,819 more in interest.

FICO Score | Annual Percentage Rate (APR) | Monthly Payment | Total Interest Paid |

|---|---|---|---|

760-850 | 2.523% | $991 | $106,686 |

700-759 | 2.745% | $1,020 | $117,179 |

680-699 | 2.922% | $1,044 | $125,668 |

660-679 | 3.136% | $1,072 | $136,077 |

640-659 | 3.566% | $1,132 | $157,463 |

620-639 | 4.112% | $1,210 | $185,505 |

Source: myFICO.com, August 31, 2020. National Averages.

Mortgage Options by Credit Score

Anyone with a credit score of 760 and up will enjoy the best available rates, easy terms, and a speedy qualification process. Lenders will not spend a lot of time reviewing these loans. Prepare for:

- Lightning-quick approval process

- Best terms available

Achieving a credit score of 760 takes time. When you get here, do everything you can to stay at this level.

If your score changes to 700-759, you could pay an extra $10,493 (Refer to the table above).

Borrowers with credit scores of 700 and up are considered A-grade to lenders. The benefits of having a score of 700 and up are:

- Lower APR

- Smaller PMI premium

- A large variety of loan programs

- Flexible terms

If your score changes to 680-699, you could pay an extra $18,982 (Refer to the table above).

If your score is at least 680, mortgage terms are far more favorable than at the tiers below. Also, at this credit score range, jumbo loans become available.

If your score changes to 660-679, you could pay an extra $29,391 (Refer to the table above).

If your score changes to 640-659, you could pay an extra $50,777 (Refer to the table above).

If your score changes to 620-639, you could pay an extra $78,819 (Refer to the table above).

Borrowers with a credit score of at least 620 have a lot more options. Lenders will present an array of loan programs, including:

- Conventional Loans (Most Popular)

- USDA Loans (Government Sponsored)

- VA Loans (Active-Duty Military and Veterans)

- FHA Loans

We will always recommend to wait and raise those credit scores. Don’t buy a home with this credit score unless you have no other options.

Having a low score or no score will mean that you are unlikely to obtain a mortgage, at least not one with favorable terms. There are lenders out there that do finance borrowers with scores 619 and below but be prepared to settle for a loan that is insured by the Federal Housing Administration (FHA). We recommend you do the following:

- Try to find a family member that has a great credit score to be on the loan with you

- Find an FHA lender that has a great reputation that will provide clear and concise terms

- Make a 10% downpayment

Understanding Terms Of Mortgages

In this section, we define the most relevant mortgage terms you need to be aware of and breakdown the Loan Estimate (LE) and Closing Disclosure (CD).

Mortgage Terms You Need to Know

Pre-Qualification

A mortgage pre-qualification generally consists of self-reported information without the lender collecting documents to verify the information. Also, lenders typically do not pull your credit report. The goal of a pre-qualification is to get a sense of where you stand financially and how much home you can generally afford. The seller and their real estate agent typically want to see that you have been pre-qualified for a mortgage before accepting any offers from you. Always be upfront with your lender when getting pre-qualified, don’t overestimate your income numbers, and don’t underestimate your liabilities. Such acts will only hurt your ability to purchase a home.

Pre-Approval

Pre-approval is the process of determining how much money you can borrow to purchase a home. Unlike a pre-qualification, a pre-approval involves the lender looking over your income statements, credit report, and assets. There are many benefits to receiving a pre-approval rather than a standard pre-qualification such as easier to shop for a home and it makes your initial offer look much stronger!

Escrow

You most likely have heard the term “escrow” before. Escrow is an account that is managed by a middleman (usually a bank) until the transaction (usually a mortgage) is complete. Mortgage escrow accounts are a holding place for your yearly property tax, insurance premiums, and/or mortgage insurance premium. Your lender will collect a small portion from you monthly (this portion is part of your mortgage payment) and will make payments on your behalf as needed.

Principal

Principal is the amount that you borrowed and have to pay back. During the first few years of your mortgage, almost always the interest portion of your mortgage payment will be larger than the principal.

Annual Percentage Rate (APR)

Most people think that APR is the same thing as an interest rate, but in reality, the APR is a much more complex calculation. The APR calculation includes the interest rate, mortgage insurance, most closing costs, discount points, and loan origination fees. The main objective of the APR is to present the borrower with a number that includes all of the items that you are paying for, not just interest.

Title Insurance

Title insurance is used to protect the home purchaser from financial loss and any legal expenses in the event of a defect being found in the title after the property has been purchased. There are a number of issues that may arise months or even years after you’ve purchased your home. Key issues that may arise are poorly executed documents, mistakes in recording of legal documents, missing heirs, tax liens or judgments, unsatisfied mortgages, and many more. Title insurance is a must!

Deed

A deed is a legal document that shows the transfer of a property from one party to the other. A deed must always be a physical document as mandated by law. Both the buyer (grantee) and the seller (grantor) must sign the deed and then the deed is recorded. Each state (or county) has its own specific recording rules. In most cases, the title company prepares the deed.

Seller Assist

Closing costs are one of the biggest obstacles when it comes to buying a home. As discussed previously, closing costs range anywhere from 2% – 5% of the loan amount. Seller assist or seller concessions help to alleviate some or in rare cases all of the buyer’s closing costs. As the name suggests, seller assist is a feature that allows the seller to contribute towards the buyers closing costs. The maximum seller assist permitted by law is 6% (of the loan amount). Seller assist is commonly negotiated at the beginning of initial contract talks between the buyer and the seller.

Fixed-Rate Mortgage

A fixed-rate mortgage carries an interest rate that remains the same through the life of the loan. With a fixed-interest rate, your monthly mortgage payments will always remain the same (if you have an escrow account for taxes and insurance, the mortgage payment may go up or down, but only for the reason stated). The majority of mortgages in the United States have a fixed-rate interest.

Underwriting

Before you, as the borrower can get your hands on the money to purchase a home, your mortgage loan goes through a process called underwriting. Underwriting is the stage of the loan where the lender reviews your income, assets, credit report, property details, and any nuances that are specific to your loan. Most lenders in the United States follow Freddie Mac/Fannie Mae guidelines when underwriting a loan.

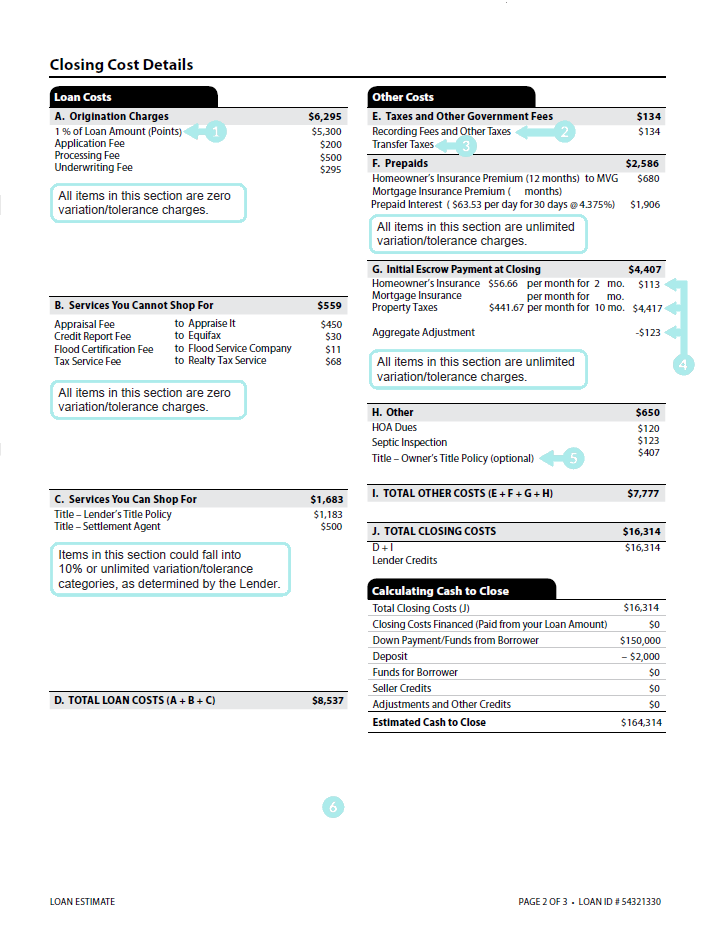

Origination Charges

Origination charges are fees that go directly to the lender and are usually pure profit for them. In most cases, origination charges will be broken down into several little fees such as origination fee, underwriting fee, application fee, document preparation fee, processing fee, and document review fee. Beware of lenders charging more than $1,000 in origination charges. If you see fees that look unusually high or out of place, confront the lender about it. And remember, origination charges are negotiable.

Home Appraisal

A home appraisal is a document that is required by the lender that shows an opinion of a home’s value that is completed by a third-party licensed appraiser. There are three types of appraisal a full appraisal, drive-by appraisal (exterior only), and an AVM (automated valuation model). Also, most appraisals are made up of pictures, comparable homes sold in the area, and a detailed description of the property. The cost of an appraisal varies anywhere from $200 (less if an AVM) to $1,000 for complex properties.

Prepaid Interest

Prepaid interest is a charge due at closing for any daily interest that accrues on your loan between the date you close on your mortgage loan and the period covered by your first monthly mortgage payment. You can find this amount on page two of the loan estimate and closing disclosure.

Loan-to-Value (LTV)

The loan-to-value is a ratio that shows the amount of your mortgage compared to the appraisal amount. The higher your down payment, the lower your loan-to-value ratio will be. Lenders use the loan-to-value ratio for many things, such as determining the interest rate, the programs that an individual qualifies for, and if mortgage insurance will be needed.

Discount Points

Discount points are fees that you pay to the lender to reduce your rate. Essentially you trade-off upfront cost for a lower rate over the life of your loan. If it’s your plan to keep your mortgage long-term (5 years or more), then paying discount points is a good option. It is also a good idea to pay discount points if your initial rate is high (4% or more). The fee that you pay depends on the mortgage amount. For example, one point on a $100,000 loan would be one percent of the loan amount, or $1,000. Two points would be two percent of the loan amount, or $2,000.

Debt-to-Income Ratio (DTI)

The debt-to-income ratio is your monthly credit obligations divided by your monthly income. For example, if your monthly liability (credit cards, auto loans, student loans, and housing payment) is $2,100 and your monthly gross income is $6,000, your DTI ratio is 35%. For most lenders in the USA, the maximum DTI is 43%.

Amortization

An amortization gives a glimpse to the borrower of how their repayment history will look over the life of the loan. Lenders include a mortgage amortization document in the loan documents. As long as there will be no pre-payment or changes in the rate, the amortization schedule will give a clear breakdown of how the payment will be applied.

Jumbo Mortgage

A jumbo mortgage is a loan that helps to finance a house that is priced higher than the conforming loan limits. Conforming loan maximum in 2020 is $510,400 in most places in the United States. Historically, the conforming loan limit rises every year as home prices tend to appreciate over time. Lenders consider jumbo mortgages to be riskier, hence they have higher underwriting standards and are priced higher as well. Jumbo mortgages are also referred to as non-conforming loans.

Fee Tolerance

Fee tolerance is simply an assigned percentage-based limit on how much a fee can rise from the loan estimate to the closing disclosure (See LE and CD breakdown below to learn more regarding what fees have what tolerance levels). The three types of fee tolerance are:

Zero-Tolerance – Fees in the zero-tolerance threshold category cannot increase from the Loan Estimate to the Closing Disclosure without being a tolerance violation. The only exception would be if a fee increase is due to one of the triggering events under the law for issuing a revised Loan Estimate.

10%-Tolerance – Fees in the 10%-tolerance threshold category can only increase by 10% cumulatively. The 10%-tolerance category includes recording fees and third-party service fees.

Unlimited-Tolerance – Fees that are not subject to any tolerance limits at all.

Adjustable-Rate Mortgage (ARM)

Unlike its fixed-rate counterpart, adjustable-rate mortgages (ARMs) do not carry the same interest rate through the life of the loan. Typically, an adjustable-rate mortgage has a “fixed” period of 3, 5, 7, or even 10 years and then it adjusts periodically. If you plan to keep your mortgage for less than short-term, then an ARM is a solid option as it most often offers a lower rate compared to a fixed-rate mortgage. A pro tip when considering an ARM is to go with a lender that offers a 3/3, 5/5, or 7/7 ARM compared to a 3/1, 5/1, or 7/1. The key difference lies in how often the rate adjusts.

Loan Servicer

Your mortgage servicer is the company that sends you your mortgage statements. Your servicer also handles the day-to-day tasks for managing your loan. Your lender may opt-in to not service loans that they originate. Lenders do this for various reasons. Some of these reasons are business-model, cost, or even convenience. Most times you as the borrower will not be affected by the lender outsourcing the servicing to a third-party company.

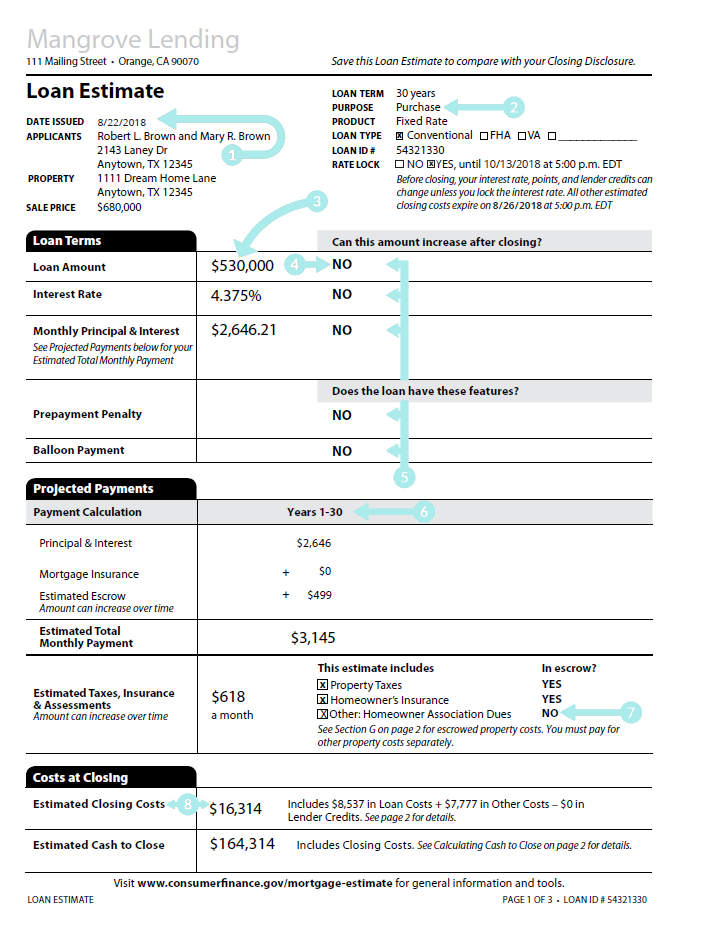

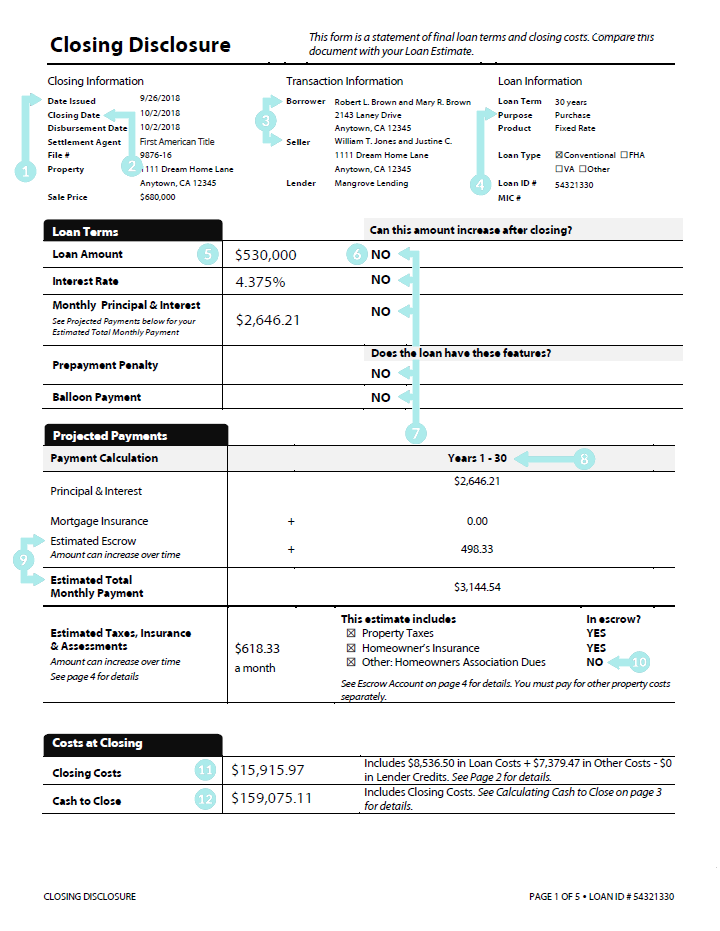

Understanding the Loan Estimate (LE)

The Loan Estimate or LE for short provides you with important information, including the estimated interest rate, monthly payment, and closing costs for the loan. The Loan Estimate also gives you information about the estimated costs of taxes and insurance (escrow), and how the interest rate and payments may change in the future. Also, the form indicates if the loan has special features that you will want to be aware of, like penalties for paying off the loan early (a prepayment penalty) or increases to the mortgage loan balance even if payments are made on time (negative amortization).

The loan estimate is issued when the lender has six items from you.

- Name

- Income

- Social Security Number

- Property Address

- Estimated Property Value

- Loan Amount

- Purchase

- Refinance

- Construction

- Home Equity Loan

Net rounded to an even dollar amount.

If YES, the loan has a negative amortization feature.

Negative amortization – even when you make payments, the amount you owe will go up because you are not paying enough to cover the interest portion of the mortgage payment.

If YES, information specific to the loan program would be shown.

Prepayment Penalty – it’s a fee that the lender charges if you pay your loan off early. Typically, in two years or less. (This feature is not common)

Balloon Payment – A balloon payment is a larger-than-usual one-time payment at the end of the loan term. A balloon feature is rare on simple primary residence mortgages.

Adjustable-rate mortgages would have up to four columns showing. This particular loan estimate is showing a fixed-rate loan.

If NO, this item is not included in the Estimated Total Monthly Payment.

HOA is the most common “Other” escrow inclusion.

Includes items paid at and before closing (click here).

Rounded Citizen Pro Reminder

Remember, the Loan Estimate is just that, an estimate. The interest rate, escrow figures, and closing costs may change. In some cases, estimated closing costs can drop as much as 10% when comparing the LE with the CD.

Zero-Tolerance

Fees in the zero-tolerance threshold category cannot increase from the Loan Estimate to the Closing Disclosure without being a tolerance violation. The only exception would be if a fee increase is due to one of the triggering events under the law for issuing a revised Loan Estimate.

10%-Tolerance

Fees in the 10%-tolerance threshold category can only increase by 10% cumulatively. The 10%-tolerance category includes recording fees and third-party service fees.

Unlimited-Tolerance

Fees that are not subject to any tolerance limits at all.

This is a fee that you pay to the lender to reduce your mortgage interest rate. Typically, 1 point (1% of the loan amount) reduces your mortgage rate by 0.25%.

Recording Fees – are fees that are typically paid to the title company for recording your mortgage and deed in the county where the property is purchased.

Other Taxes – Any other taxes that are associated with purchasing the property.

This is the tax that is paid when the passing of title to the property occurs. Think of it as a sales tax that is paid when purchasing a product. This tax varies widely. It can be as low as 1% or as high as 4.5%.

These payments can be viewed as the initial “investment” into your escrow account. The lender typically looks at this initial deposit as a cushion.

It’s an insurance policy that offers protection in an event if someone sues you and states that they have a claim to the property before you purchased it.

Additional Tables appear here if the loan program includes Adjustable Payment (AP) or Adjustable Interest Rate (AIR) features.

The loan estimate is not required to be signed. If you do end up signing the loan estimate, it’ll be only be considered as acknowledgment of receipt.

Understanding the Closing Disclosure (CD)

A Closing Disclosure is very similar to the loan estimate. The difference is that the closing disclosure provides final details regarding your mortgage loan. It includes the loan terms, your projected monthly payments, and how much you will pay in fees and other costs to get your mortgage (closing costs).

The closing disclosure is required to be sent by the lender three days before the closing occurs.

The closing date or consummation date is the day that the closing on the house occurs. For purchases, this date is typically set in the agreement of sale when the buyer and seller agree on initial terms. For refinances, the closing date is set by the lender and is generally much more flexible.

Name and current address of the buyer(s) and the seller(s).

- Purchase

- Refinance

- Construction

- Home Equity Loan

Net rounded to an even dollar amount.

If YES, the loan has a negative amortization feature.

Negative amortization – even when you make payments, the amount you owe will go up because you are not paying enough to cover the interest portion of the mortgage payment. Lenders typically do not allow this feature.

If YES, information specific to the loan program would be shown.

Prepayment Penalty – it’s a fee that the lender charges if you pay your loan off early. Typically, in two years or less. (This fee is not common)

Balloon Payment – A balloon payment is a larger-than-usual one-time payment at the end of the loan term. A balloon feature is rare on simple primary residence mortgages.

Adjustable-rate mortgages would have up to four columns showing. This particular closing disclosure is showing a fixed-rate loan.

The term “Estimated” is used because the Escrow amount can change over time. On average, property taxes go up by about 4% each year (this amount varies state to state).

If NO, this item is not included in the Estimated Total

Monthly Payment.

HOA is the most common “Other” escrow inclusion.

Includes items paid at and before closing (click here).

The full amount required to close on the home. Including closing costs, taxes, remaining downpayment, and other miscellaneous costs.

The actual amount required for closing may differ from this Cash to Close amount if the Lender does not allow a title premium adjustment on Page 3, Sections L and N.

This is a fee that you pay to the lender to reduce your mortgage interest rate. Typically, 1 point (1% of the loan amount) reduces your mortgage rate by 0.25%.

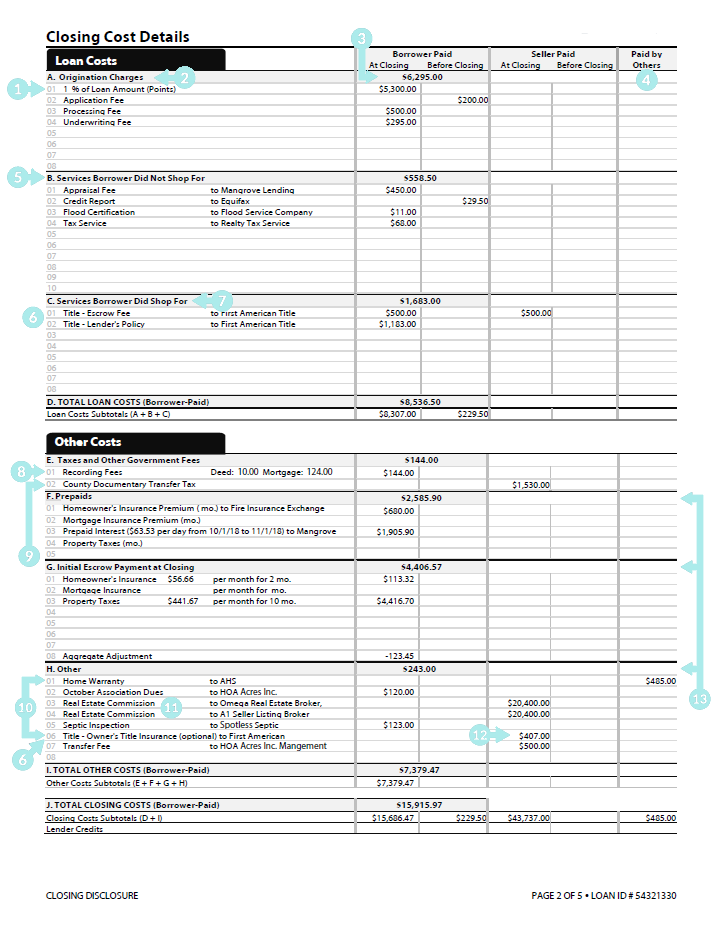

There are several origination charges that the lender can charge you. Some examples of origination charges are:

- Discount Points

- Application Fee

- Commitment Fee

- Processing or Document Preparation Fee

- Underwriting Fee

Origination Charges are Zero-Tolerance.

Fees in the zero-tolerance threshold category cannot increase from the Loan Estimate to the Closing Disclosure without being a tolerance violation.

Unlike the HUD-1 (closing disclosure predecessor), which listed the subtotals at the bottom, the closing disclosure lists the section subtotals at the top.

Individual or entity other than the seller or buyer who paid the fee or charge.

This section of the closing disclosure includes charges that the borrower did not shop for, such as appraisal fee, credit report, flood certification, tax servicing, and other servicing fees that the lender may incur.

Services Not Shopped For are 10%-Tolerance

Fees in the 10%-tolerance threshold category can only increase by 10% cumulatively. The 10%-tolerance category includes recording fees and third-party service fees.

Any item that is a component of or related to the title insurance or settlement must contain a description that begins with the word “Title”.

This section of the closing disclosure includes charges that the borrower did shop for typically 3rd party services, such as pest inspection, surveys, title services (title insurance, settlement agent, and title search fees).

Services Shopped For are Unlimited-Tolerance

Fees that are not subject to any tolerance limits at all.

There are other costs that could be a part of your mortgage, including taxes and government fees, prepaids, initial escrow payment at closing, initial escrow payments at closing, and more.

Recording Fees – are fees that are typically paid to the title company for recording your mortgage and deed in the county where the property is purchased.

Recording Fees are 10%-Tolerance

Fees in the 10%-tolerance threshold category can only increase by 10% cumulatively. The 10%-tolerance category includes recording fees and third-party service fees.

There are other costs that could be a part of your mortgage, including taxes and government fees, prepaids, initial escrow payment at closing, initial escrow payments at closing, and more.

This is the tax that is paid when the passing of title to the property occurs. Think of it as a sales tax that is paid when purchasing a product. This tax varies widely. It can be as low as 1% or as high as 4.5%.

Transfer Taxes are Zero-Tolerance.

Fees in the zero-tolerance threshold category cannot increase from the Loan Estimate to the Closing Disclosure without being a tolerance violation.

There may be other expenses that need to be paid at closing, including homeowners association fees, a home inspection fee, home warranty fee, real estate commissions, and owner’s title insurance.

If paid Borrower, must include (Optional) at end of the description. If paid Seller, (Optional) may be shown but is not required.

Any item that is a component of or related to the title insurance or settlement must contain a description that begins with the word “Title”.

The full real estate commission must be shown regardless of who is holding the earnest money deposit (initial home deposit). Any additional charges for services provided (e.g. Admin Fee) must be itemized separately.

In states where a reduced premium is charged for the simultaneous issue of lender’s and owner’s policies, the premium shown in Section H will not equal the actual rates in that state. If Lender allows a title premium adjustment between Borrower and Seller, it will be shown on Page 3, Sections L and N. If Lender does not allow the title premium adjustment, Cash To/From Borrower and Seller will not be accurate.

Charges in sections F, G, and H are – Unlimited Tolerance.

Fees that are not subject to any tolerance limits at all.

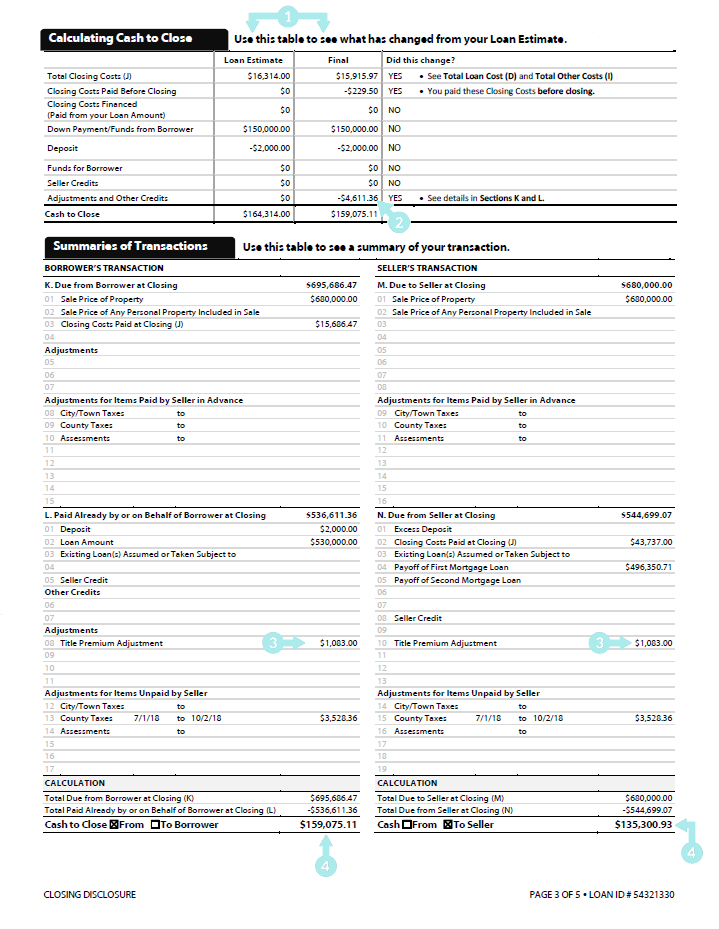

This section allows for a comparison between the loan estimate and the closing disclosure. The amounts shown in the loan estimate column are rounded. The amounts shown in the final column are not rounded. If you find that the cash to close amount in the final column is larger than in the loan estimate column, contact your lender immediately and ask for an explanation as to why this occurred.

This figure is an aggregate of debits and other credits shown in Sections K and L.

This example shows:

L.08 – L.13

$1,083.00 – $3,528.36 = $4,611.36.

In states where a reduced premium is charged for the simultaneous issue of lender’s and owner’s policies, the premium shown in Section H will not equal the actual rates in that state. If Lender allows a title premium adjustment between Borrower and Seller, it will be shown on Page 3, Sections L and N. If the Lender does not allow the title premium adjustment, Cash To/From Borrower and Seller will not be accurate.

Cash to close reflects the full amount you need to bring to closing and includes any deposits you’ve already paid to the seller. It will also include how much money, if any, the seller is planning to pay toward your closing costs – known as a seller assist. These are closing costs that you negotiate with the seller to pay. Seller assist can range anywhere from 1% to 6%.

Additional Tables appear here if the loan program includes Adjustable Payment (AP) or Adjustable Interest Rate (AIR) features.

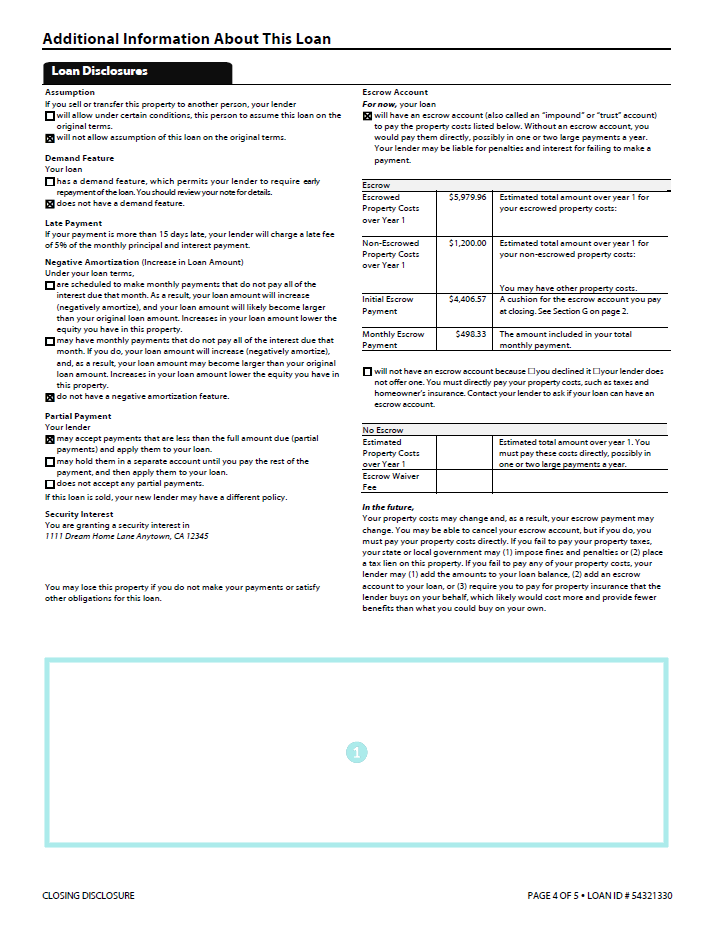

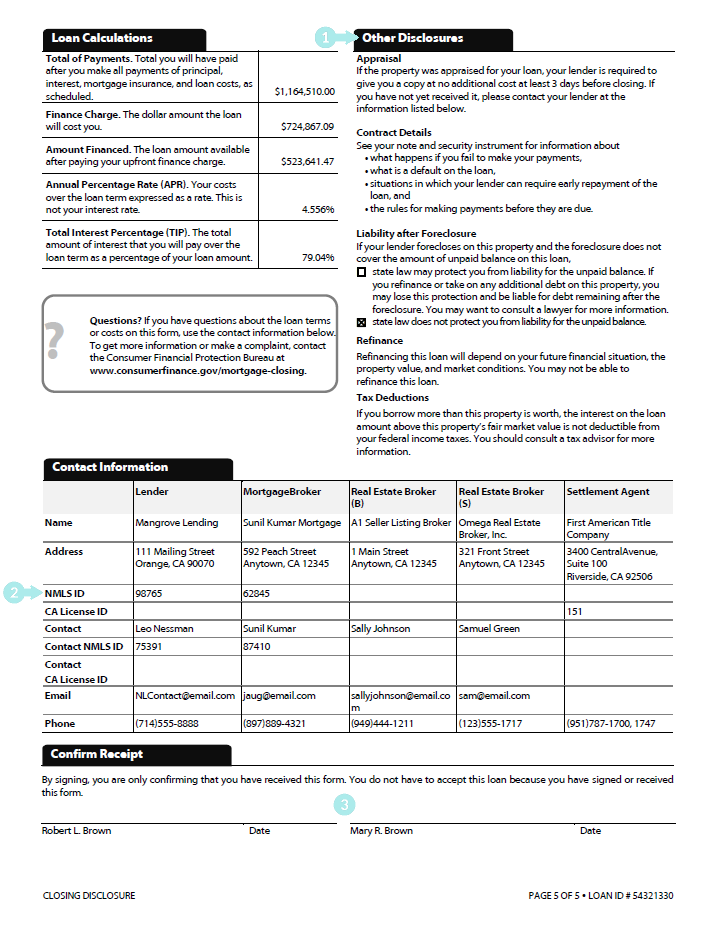

The Other Disclosures section contains all of the other important disclosures that were not mentioned on page four. If you see something that doesn’t look right, contact your lender immediately. They are required to provide you with an explanation.

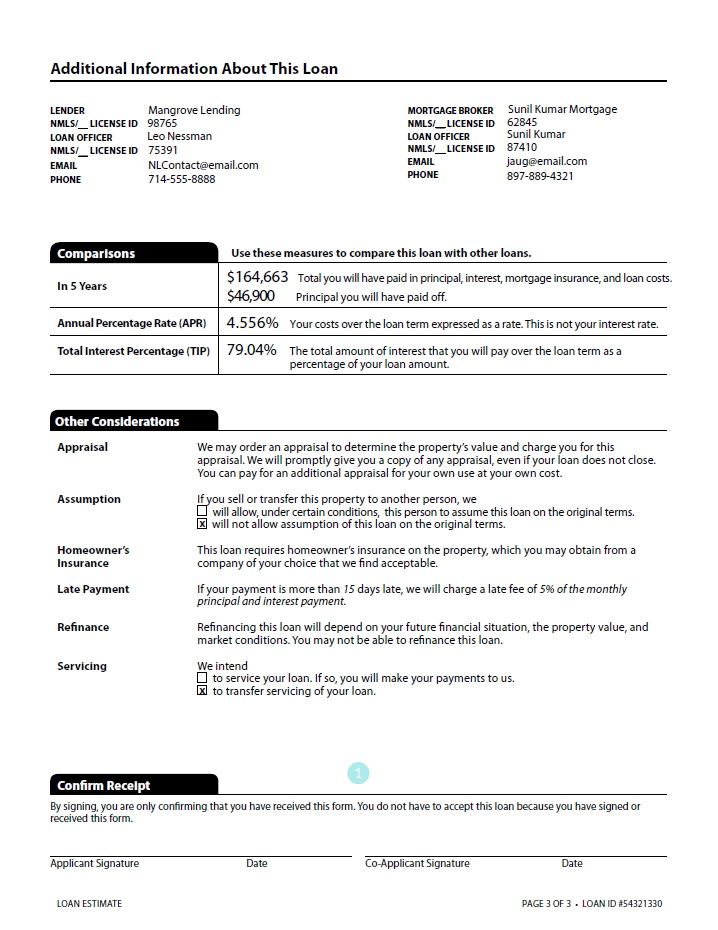

The NMLS Unique Identifier is the number permanently assigned by the Nationwide Mortgage Licensing System & Registry (NMLS) for each company, branch, and individual that maintains a single account on NMLS. The NMLS Unique Identifier (“NMLS ID”) improves supervision and transparency in the residential mortgage markets by providing regulators, the industry, and the public with a tool that tracks companies and individuals across state lines and over time.

If you’re questioning the integrity of the lender and/or loan originator that you’re working with, ask for their NMLS ID number. If the entity you’re working with does not have an NMLS ID, we suggest you stay away from such lenders.

The lender may not require a signature. Signature is an acknowledgment of receipt, not acceptance of the loan.

Loan Types

Every borrower is unique. This is why many mortgage loan types exist. In this section, we go over the four main mortgage loan types in circulation today.

Conventional Mortgages

Conventional Mortgage – is a mortgage loan that is not backed by the U.S. government. Conventional mortgages are issued by:

- Banks

- Credit Unions

- Private Mortgage Companies

The above-mentioned issuers typically follow Fannie Mae and/or Freddie Mac lending guidelines (unless it is a non-conforming loan). Some of the lending guidelines include:

- LTV Ratios (No higher than 97%)

- Credit Score (No lower than 620)

- Loan Purpose

- Amortization Type

- Property Type and Number of Units

- Debt-to-Income Ratio (No higher than 45%)

- Financial Reserves

The types of individuals that apply for conventional mortgages are borrowers with a great income, good credit, and have some sense of financial security. In addition, conventional mortgages tend to have higher out-of-pocket expenses when closing on the loan (unless the lender is offering some kind of closing cost assistance).

Conventional Mortgages fall into two categories: conforming and non-conforming loans (jumbo loans).

Simply put, conforming loans follow Fannie Mae and Freddie Mac guidelines and non-conforming loans do not. Currently, the conforming loan limit for single-family homes is $510,500 ($765,600 in Alaska, Guam, Hawaii, and the U.S. Virgin Islands) and the non-conforming loan limit is $765,600. To add, since non-conforming loans do not follow the above-mentioned guidelines, they are much more difficult to qualify for.

FHA Mortgages

FHA Mortgage – is a mortgage that is insured by the Federal Housing Administration (FHA). This type of mortgage loan is designed to provide financing to those borrowers who require that extra bit of help. The FHA insures the mortgage which gives lenders protection and allows lenders to issue such mortgages. FHA mortgages are issued by banks, credit unions, and private mortgage companies. FHA loans offer the following benefits:

- Downpayment as low as 3.5%

- Credit scores as low 500

- Lower PMI payments

- Flexible rules on gift funds

- Easy to qualify for

There are drawbacks to FHA loans. Some of those drawbacks are:

- Increased closing costs (FHA fees)

- Upfront PMI premium payment

- Stringent property requirements

- Interest rates tend to be higher

The Federal Housing Administration (FHA) also offers many loan options to tailor fit every single borrower. Some of the most common FHA loan options are:

- Adjustable-Rate Mortgages

- Basic Home Mortgage Loan 203(B)

- Condominium Mortgages

- 203(K) Rehabilitation Mortgages

- Urban Renewal Mortgages

Unlike conventional mortgages, FHA insured mortgages have loan limits. The limit varies from county to county. For 2020, the loan limit ranges from $331,760 to $765,600. Click here to browse limits by county.

VA Mortgages

VA Mortgage – is a mortgage loan available to service members, veterans, and their families through the United States Department of Veteran Affairs. The VA sets the terms of the mortgage and guarantees a portion of the loan allowing the lender to offer more favorable terms. VA mortgages are issued by banks, credit unions, and private mortgage companies. The VA themselves are not a lender.

Some of the generous VA loan benefits include:

- 0% down payment

- No PMI (private mortgage insurance) required

- The federal government guarantees a part of the loan

- No prepayment penalty (click here)

- Lower closing costs

USDA Mortgages

USDA Mortgage – is a mortgage loan that offers a 0% down payment for eligible rural and suburban homebuyers. USDA mortgage loans are issued by the Rural Development Guaranteed Housing Loan Program. Most people think that the program is hard to qualify for, here you can see the income requirements based on where you live.

The USDA consists of three loan programs. They are: